Impact of military operations in Iran on the redistribution of energy from the Persian Gulf

Middle East redistributed energy flows map. Source: Ignacio Mendez, Security Analyst Intern, Risk Intelligence

27 April 2026

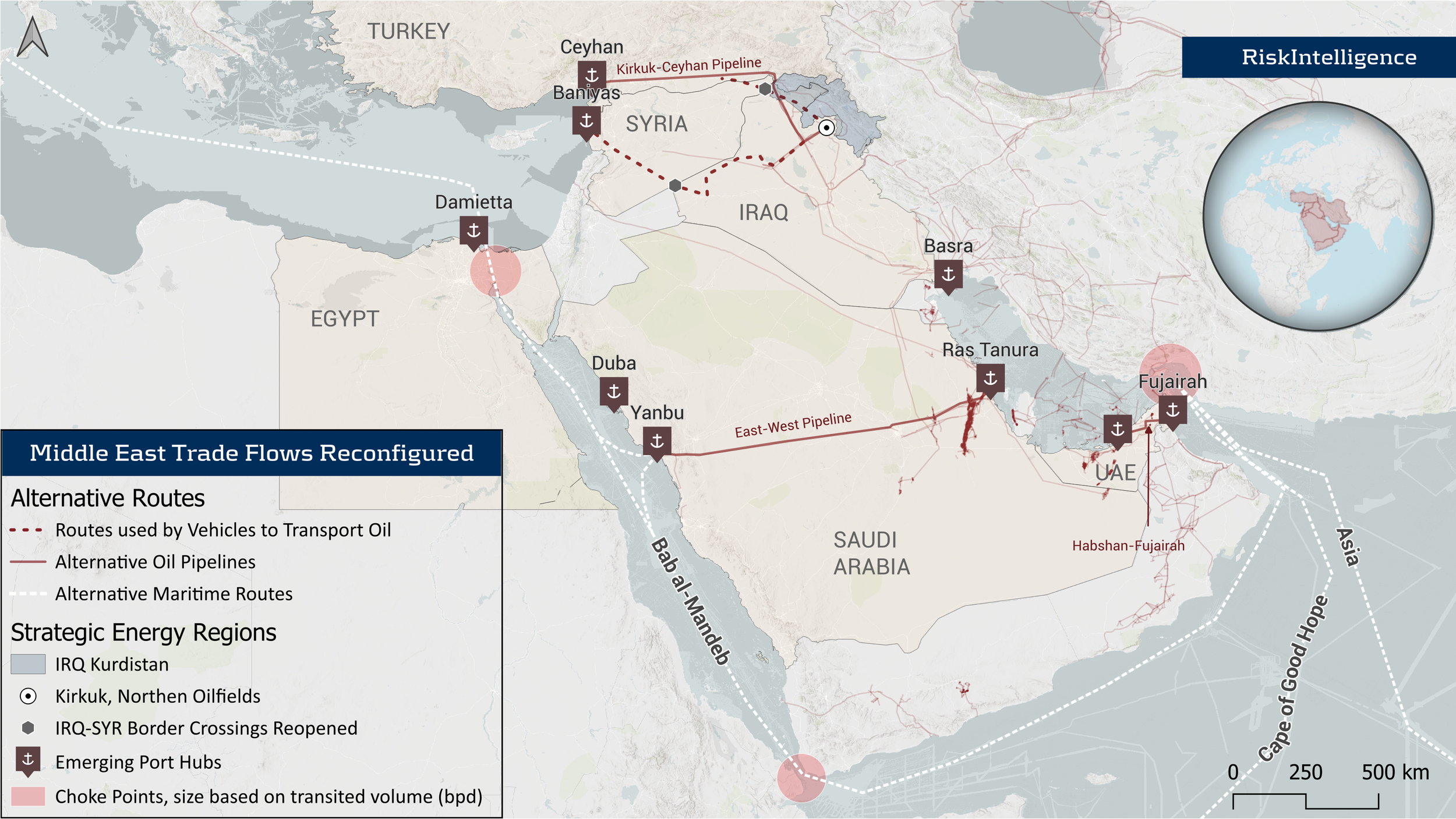

The Strait of Hormuz remains a choke point in the global energy supply chain. Heightened threats have pushed exporters to rely increasingly on alternative routes and ports, including southern Gulf terminals, pipeline-linked outlets, and longer maritime detours. These new routes face elevated security, operational and cost risks, disproportionately affecting countries most dependent on rerouted energy exports.

By Ignacio Mendez, Security Analyst Intern

After the outbreak of US and Israeli military operations in the Middle East on 28 February, threats to maritime transit through the Strait of Hormuz have increased significantly across multiple dimensions. This escalation has adversely affected the export capacity of Gulf nations, limiting their ability to export essential materials and raw commodities that are vital for daily activities. The initial economic repercussions caused by this severe disruption in the supply chain from the region are now evident, as reflected in elevated volatility and rising prices for petroleum-based products. As one of several indicators, Brent crude prices rose from 66 USD per barrel in January, to reach 100 USD per barrel in April. To mitigate the threat of a world supply crisis, and avoid the destabilization of Gulf economies, new alternative maritime and land-based routes are emerging, to diversify and reduce reliance on Hormuz.

Geographically, the Persian Gulf is an enclosed body of water, and the Strait of Hormuz is the only maritime access route for the Gulf states. Crude oil, liquefied natural gas (LNG), fertiliser feedstocks, led by sulphur supply, aluminium, and helium, ranked by their share of total trade, are the primary exports transported through the Strait. The trade disruption affects the economies of Asian, European, and African importers more than others, with China, Japan, India, South Korea, Morocco, South Africa, Germany and France among the most exposed.

As an alternative to Strait, core Gulf producers have identified operational channels capable of reallocating a portion of their oil flows. The United Arab Emirates (UAE), through the Habshan-Fujairah pipeline connecting Abu Dhabi’s coast to Fujairah oil facilities, has redistributed 50-60% of UAE crude oil exports. Saudi Arabia employs the East-West pipeline to direct its crude oil towards its Yanbu oil facility on the Red Sea, which has now assumed a key role of redirecting 85-90% of Saudi oil crude exports with shipments channelled through the Mediterranean port of Damietta in Egypt.

Iraq, with approximately 90% of its government revenue reliant on oil exports, has had to reroute crude oil shipments from both northern fields and its southern Basra fields by reactivating its two primary, high-volume routes. The initial pipeline route begins in Kirkuk, northeast Iraq, and terminates at Ceyhan, situated in southeastern Anatolia, Turkey. Under the Baghdad–Erbil agreement reached on 17 March this pipeline was authorised for the transit of crude oil across IRQ Kurdish territory with a current throughput of 250-300,000 bpd. The second route traverses Syria from central Iraq to the port city of Baniyas via the Al‑Waleed border crossing. Due to the deteriorated condition of the connecting pipeline, oil is currently transported by road, requiring an average transit time of around three days and involving approximately 600 tanker trucks per day, which significantly increases transit risk given the potential security threats. In parallel, a third, non‑major route, has also been activated, relying on trucked oil flows crossing into Turkey via the Rabya border point.

Maritime chokepoints sit at the core of the current tensions, with uncertainty over whether the future status of the Strait of Hormuz. As a result, alternative supply routes for Europe, Asia and Africa are being assessed ongoing, including rerouting exports via the Bab al‑Mandeb Strait or through the Suez Canal, options exposed to potential Houthi threats or traffic load related problems respectively. A longer fallback route around the Cape of Good Hope avoids these choke points but entails higher transport costs, although is currently assessed as low risk. The ability of new logistics hubs to manage added volume and local security conditions will decide if rerouted paths are sustainable.

MARITIME SECURITY REPORTS:

Our Risk Intelligence reports provide valuable insights to assess the risks of specific routes and support decision-making with detailed threat assessments.

The Voyage Risk Assessment focuses on a vessel’s specific route and offers an independent third-party perspective on the necessary security measures. The Monthly Intelligence Report delivers comprehensive analysis of recent incidents and a threat assessment for three key regions, available via subscription.